Tutorial 5: Lagged regressors#

Lagged regressors are used to correlate other observed variables to our target time series. For example the temperature of the previous days might be a good predictor of the temperature of the next day.

They are often referred to as exogenous variables or as covariates. Unlike future regressors, the future of a lagged regressor is unknown to us.

At the time \(t\) of forecasting, we only have access to their observed, past values up to and including \(t − 1\).

First we load a new dataset which also contains the temperature.

[2]:

import pandas as pd

# Load the dataset for tutorial 4 with the extra temperature column

df = pd.read_csv("https://github.com/ourownstory/neuralprophet-data/raw/main/kaggle-energy/datasets/tutorial04.csv")

df.head()

[2]:

| ds | y | temperature | |

|---|---|---|---|

| 0 | 2015-01-01 | 64.92 | 277.00 |

| 1 | 2015-01-02 | 58.46 | 277.95 |

| 2 | 2015-01-03 | 63.35 | 278.83 |

| 3 | 2015-01-04 | 50.54 | 279.64 |

| 4 | 2015-01-05 | 64.89 | 279.05 |

[3]:

# Optional:To align the scale of temperature with the energy price, we convert it to Farenheit:

df["temperature"] = (df["temperature"] - 273.15) * 1.8 + 32

[4]:

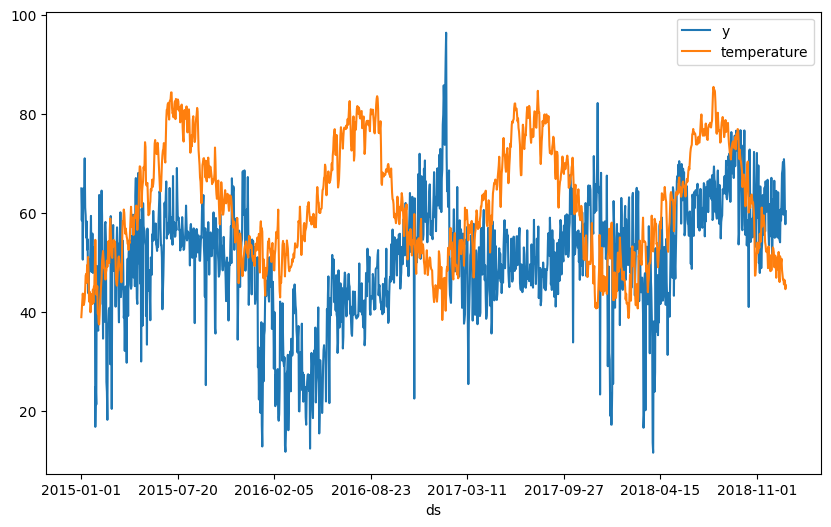

fig = df.plot(x="ds", y=["y", "temperature"], figsize=(10, 6))

From the data we can see that there is a weak inverse relationship of electricity price to temperature. We start with our model from the previous tutorial and then add temperature as a lagged regressor to our model.

[ ]:

from neuralprophet import NeuralProphet, set_log_level

# Disable logging messages unless there is an error

set_log_level("ERROR")

# Model and prediction

m = NeuralProphet(

n_changepoints=10,

yearly_seasonality=True,

weekly_seasonality=True,

daily_seasonality=False,

n_lags=10, # Autogression

)

m.set_plotting_backend("plotly-static")

# Add temperature of last three days as lagged regressor

m.add_lagged_regressor("temperature", n_lags=3)

# Continue training the model and making a prediction

metrics = m.fit(df)

forecast = m.predict(df)

[16]:

# set plotting to focus on forecasting horizon 1 (the only one for us here)

m.highlight_nth_step_ahead_of_each_forecast(1)

m.plot(forecast)

[15]:

# show the component's forecast contribution

m.plot_components(forecast, components=["lagged_regressors"])

We see that the temperatur impact the forecasted price by few units. Compared to the overall price fluctuations, the temperature impact seems minor, but not insignificant.

[17]:

# visualize model parameters of lagged regression

m.plot_parameters(components=["lagged_regressors"])

The model learns a different weights for each of the lags, which may also capture changes in the direction of temperature.

Let us explore how our model improved after adding the lagged regressor.

[20]:

metrics.tail(1)

[20]:

| MAE | RMSE | Loss | RegLoss | epoch | |

|---|---|---|---|---|---|

| 172 | 4.936666 | 6.578746 | 0.00533 | 0.0 | 172 |

[7]:

df_residuals = pd.DataFrame({"ds": df["ds"], "residuals": df["y"] - forecast["yhat1"]})

fig = df_residuals.plot(x="ds", y="residuals", figsize=(10, 6))